The Subscriber Reckoning: Netflix's Growth Myth Shatters

The Setup

What the world looked like at entry

In April 2022, Netflix reported what the market had long considered unthinkable: its first subscriber loss in over a decade. The streaming giant shed 200,000 subscribers in Q1 and warned that Q2 would bring losses of 2 million more. The stock, already battered during a broader growth-to-value rotation, cratered from $340 to $215.52 in a single week—a 37% collapse that wiped out over $50 billion in market capitalization. Bill Ackman's Pershing Square, which had bought $1.1 billion in NFLX shares just three months earlier, dumped the entire position at a $400 million loss within 48 hours of the earnings report.

But the panic overshot. While nearly every institutional narrative turned apocalyptic—"Netflix is the new Blockbuster," "the streaming wars are unwinnable"—the company's fundamentals told a more nuanced story. Revenue was still growing. The subscriber loss was heavily skewed by Russia's forced shutdown (700,000 accounts). And management was already pivoting: announcing an ad-supported tier and a password-sharing crackdown that would eventually become the company's most successful growth catalysts. The market was pricing in a death spiral while Netflix was reloading.

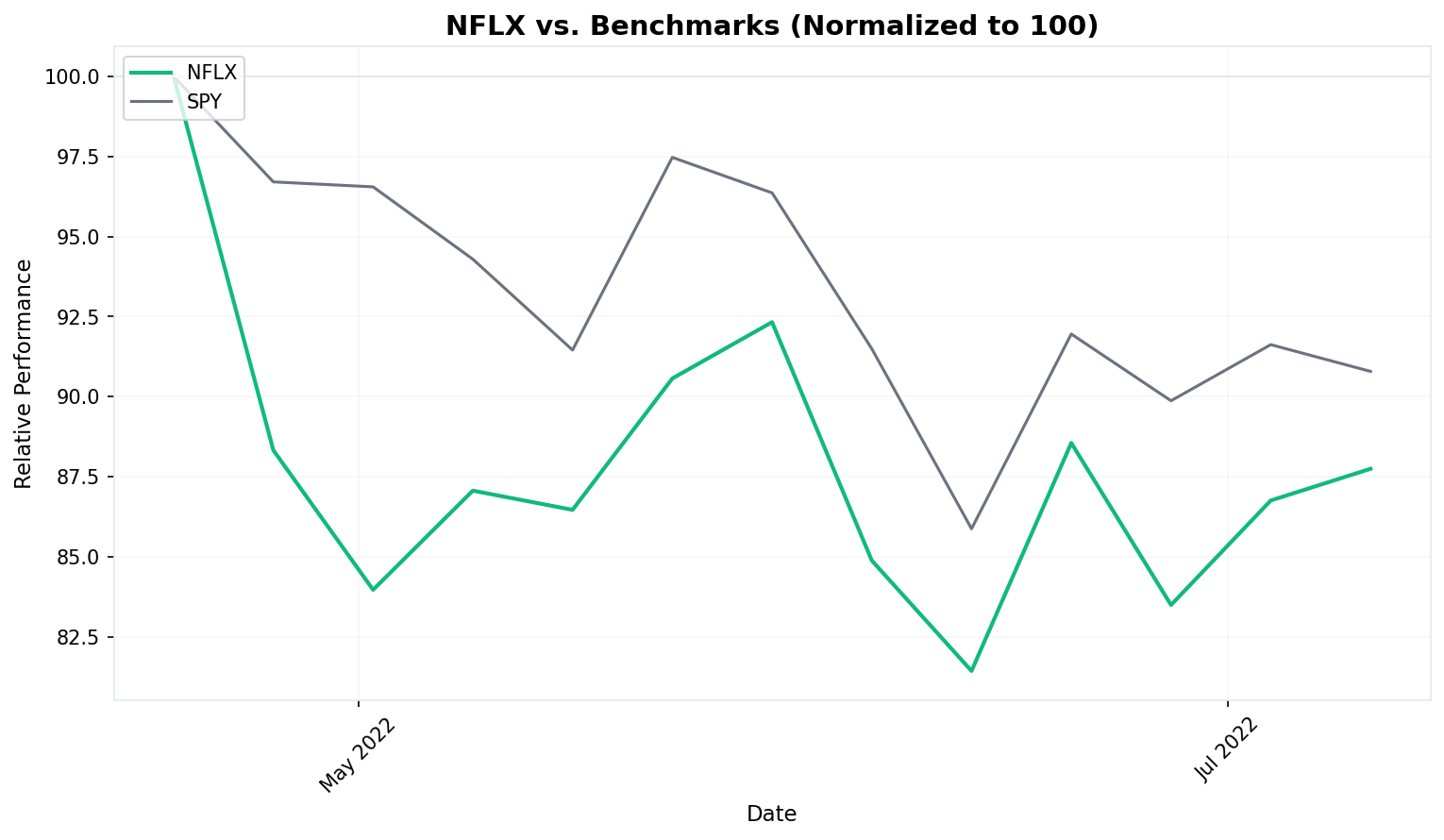

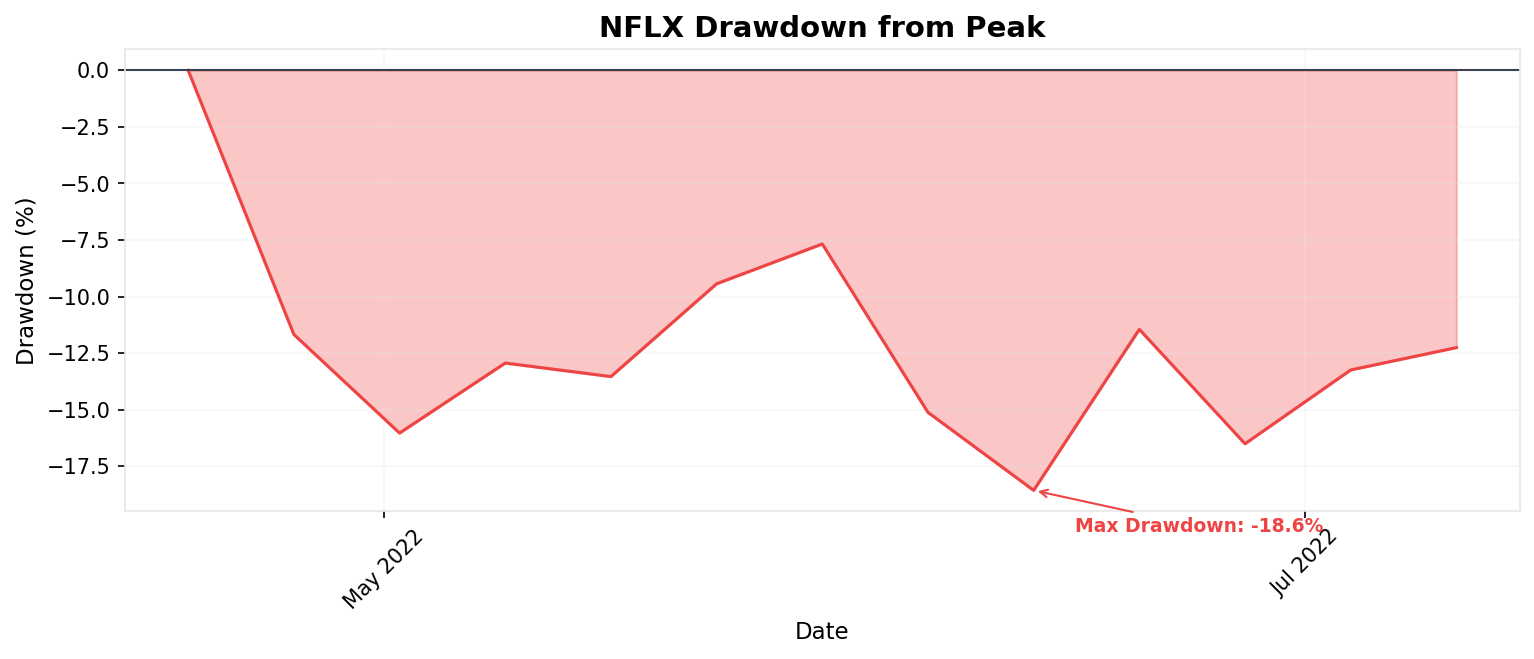

This case study tracks a three-month hold from the post-earnings collapse through a choppy recovery, ultimately capturing a modest +2.28% return. That headline number underwhelms until you measure it against the S&P 500's -7.26% decline over the same period, producing +9.54% of alpha. The trade survived a gut-wrenching -18.6% drawdown along the way—a test of conviction that separated those who understood the overreaction from those who capitulated alongside Ackman.

MACRO REGIME

- The Federal Reserve had begun its most aggressive rate-hiking cycle in decades, with the first 25bp increase in March 2022

- Inflation was running above 8%, forcing a hawkish pivot that punished long-duration growth assets

- The Nasdaq Composite was already down over 20% from its November 2021 highs

- A severe growth-to-value rotation was underway; the MSCI World Growth Index would fall nearly 30% for the year

- Rising rates were compressing valuations on unprofitable and high-multiple tech names across the board

COMPANY SETUP

- Netflix had missed subscriber expectations in Q4 2021, adding only 8.3 million vs. guidance of 8.5 million

- Stock fell from a high of $700.99 in November 2021 to $397.50 by the week of January 17—a 43% decline before Q1 earnings

- OHLC data showed sustained selling pressure: from $397.50 on January 17 to $341.13 by April 11, a relentless grind lower

- Price had breached $340 support (week of March 7, closing at $340.32) before a brief bounce to $380.60

- Bill Ackman's Pershing Square disclosed a $1.1 billion position (~3.1 million shares) in January 2022, briefly boosting sentiment

- Netflix was trading at roughly 25x forward earnings, still elevated versus the market's shifting preference for profitability

SECTOR MOMENTUM

- Disney+ had reached 129.8 million subscribers, growing at 33% year-over-year

- HBO Max, Paramount+, Apple TV+, and Peacock were all scaling, fragmenting the subscriber pie

- The streaming market was shifting from "growth at all costs" to concerns about profitability

- Content costs were spiraling across the industry, with every major studio pouring billions into original programming

- Investors were beginning to question whether any streaming service besides Netflix could be sustainably profitable

SENTIMENT

- Analyst consensus was mixed-to-bearish heading into Q1 earnings; several firms had cut price targets

- Retail sentiment remained relatively positive, with "buy the dip" narratives circulating on social media

- Short interest had been climbing steadily since November 2021

- The stock had already fallen 51% from its all-time high, leading some to argue the bad news was priced in

Entry Point

The thesis and the position

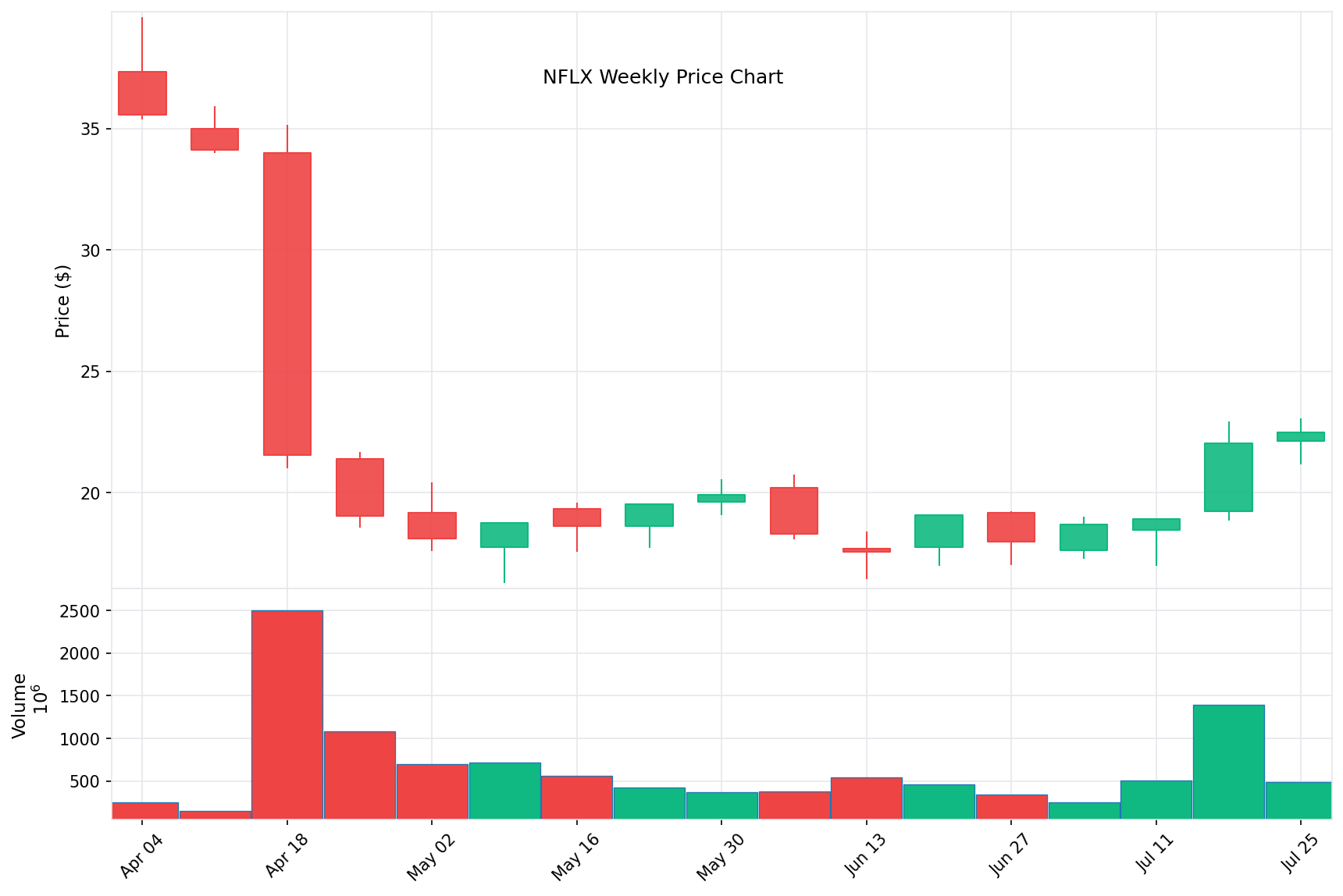

A trader entering Netflix on April 18 was buying into the teeth of a panic. The Q1 earnings report, released after the close on April 19, would confirm the market's worst fear—a subscriber loss—and send the stock down another 35% overnight. But the entry week's OHLC tells the story: the stock opened at $340.00, plunged to an intraweek low of $210.05, and closed at $215.52. The collapse was historic, but it was also the kind of indiscriminate selling that creates opportunity.

The contrarian thesis rested on several observable facts. First, Netflix's subscriber loss was significantly distorted by the shutdown of Russian operations (700,000 accounts). Excluding Russia, the company would have added 500,000 subscribers. Second, Netflix was still generating $7.87 billion in quarterly revenue with 30% operating margins—this was not a broken business. Third, the competitive moat was deeper than the narrative suggested: Netflix's content library and recommendation engine had no real peer, and competitors were losing billions trying to match its scale. Fourth, management was signaling two major strategic pivots—an ad-supported tier and a password-sharing crackdown—that could unlock enormous untapped revenue.

The risk was straightforward: if subscriber losses accelerated in Q2 (Netflix guided for a 2 million loss), the stock could fall significantly further. The market was in no mood to give benefit of the doubt, and the broader macro environment was hostile to any stock that smelled like "growth."

Before continuing: Consider what you would have done.

The Journey

From entry to exit

Key Events

| Date | Event | Category | Stock Reaction |

|---|---|---|---|

| Apr 18, 2022 | Entry week opens at $340.00; Q1 earnings reveal 200K subscriber loss | Earnings | Collapsed to $215.52 close (-37% intraweek) |

| Apr 20, 2022 | Bill Ackman sells entire $1.1B NFLX stake at ~$400M loss | Capitulation | Selling pressure intensified; next week closed $190.36 |

| Apr 25, 2022 | Stock hits post-earnings continuation low, closes week at $190.36 | Sentiment | Further -11.7% from entry close |

| May 10, 2022 | Netflix confirms ad-supported tier and password crackdown plans for 2022 | Strategic | Modest stabilization; stock at $180.97 that week |

| May 9, 2022 | Intraweek low of $162.71—the absolute bottom | Capitulation | Maximum pain: -24.5% below entry |

| Late May 2022 | Stranger Things Season 4 launch drives engagement spike | Content | Stock rallied from $186.35 to $198.98 over two weeks |

| Jun 6, 2022 | Broader market selloff resumes; CPI prints 8.6% (40-year high) | Macro | Stock fell back to $182.94 |

| Jun 13, 2022 | Market fears peak; Fed delivers 75bp rate hike; NFLX closes at $175.51 | Macro | Worst closing low of the trade period (-18.6% from entry) |

| Jun 23, 2022 | Netflix announces Microsoft partnership for ad-supported tier | Strategic | Sentiment improved; stock at $190.85 that week |

| Jul 13, 2022 | Microsoft partnership details emerge; ad tier optimism builds | Strategic | Stock climbed to $189.11 |

| Jul 19, 2022 | Q2 earnings: lost 970K subs vs. 2M guided—far better than feared | Earnings | Stock surged; exit week close $220.44 |

How It Unfolded

Phase 1: The Collapse (April 18 - April 25) The entry week was one of the most violent single-stock moves in recent memory. Netflix opened at $340.00 on Monday, reported earnings Tuesday evening, and the stock gapped down to $210.05 intraweek before closing at $215.52. The following week brought continuation selling, with Ackman's highly publicized exit adding fuel to the fire. The stock closed at $190.36, marking a cumulative -11.7% decline from the already-devastated entry price. The narrative was uniformly bearish: Netflix was "the next Blockbuster."

Phase 2: Capitulation and Basing (May 2 - May 23) The stock ground to its absolute low of $162.71 during the week of May 9—a harrowing -24.5% below entry. But something shifted beneath the surface. Netflix confirmed concrete plans for an ad-supported tier and a password-sharing crackdown, signaling that management was not in denial about the challenges. Weekly closes stabilized in the $180-$195 range. Volume began to normalize. The panic was exhausting itself.

Phase 3: The Stranger Things Bounce (May 23 - June 6) The launch of Stranger Things Season 4 in late May reminded the market that Netflix still had unmatched cultural reach. The show became the most-watched English-language series in Netflix history. The stock rallied from $186.35 to $198.98 over two weeks, approaching the $200 psychological level. For the first time since the earnings disaster, buyers appeared to have conviction.

Phase 4: The Macro Gut-Check (June 6 - June 27) The rally stalled when the broader market got hit by a devastating June CPI print of 8.6% and the Fed's first 75bp rate hike. Netflix, as a high-beta growth name, was dragged down with everything else. The stock fell to its worst closing low of $175.51 on June 13, then rebounded to $190.85 the following week as the Microsoft ad-tier partnership was announced. This phase tested whether holders were in the trade for Netflix-specific reasons or just riding market beta.

Phase 5: Recovery Into Q2 Earnings (July 4 - July 18) As Q2 earnings approached, a subtle shift in expectations became the trade's catalyst. The 2-million subscriber loss guidance from April had become the consensus anchor, and any result better than catastrophic would be received as good news. Netflix reported a loss of 970,000 subscribers—bad in absolute terms, but less than half the feared number. Revenue grew 9% year-over-year. The stock surged during the exit week, closing at $220.44 after reaching an intraweek high of $229.35.

Exit

- Date: July 18, 2022

- Price: $220.44

- Context: Netflix's Q2 earnings on July 19 confirmed what contrarians had suspected: the subscriber bleeding was far less severe than the apocalyptic guidance suggested. The 970,000 net losses represented a beat of more than 1 million subscribers versus the company's own Q2 forecast. Management guided for 1 million subscriber additions in Q3, signaling the inflection was near. The stock's exit-week surge to $220.44 (with an intraweek high of $229.35) provided a clean exit point as the thesis played out.

Price Action

The trade in chart form

Results

The final accounting

Over the same April 18 to July 18 period, the S&P 500 (SPY) fell from $426.04 to $395.09, a decline of -7.26%. Netflix's +2.28% return produced +9.54% of alpha against the broad market. This outperformance is particularly notable given that it occurred during one of the worst stretches for growth stocks in 2022, with the Nasdaq entering deep bear market territory.

The alpha generation was concentrated in two periods: the initial post-capitulation bounce (when Netflix stopped falling faster than the market) and the Q2 earnings beat (when Netflix surged while the market remained flat). During the mid-trade drawdown in June, Netflix fell roughly in line with SPY, suggesting the drawdown was primarily macro-driven rather than Netflix-specific deterioration.

Lessons

What the trade revealed

What Worked

-

Buying into maximum pessimism. The entry came during the week of the worst single-stock earnings reaction in Netflix's history. Ackman's public capitulation, wall-to-wall bearish coverage, and a 37% intraweek collapse created the conditions for a sentiment floor. When a billionaire sells $1.1 billion in stock at a $400 million loss on national television, you're buying from the weakest hands.

-

Separating narrative from numbers. The "Netflix is dying" narrative ignored that the company still generated $7.87 billion in quarterly revenue with healthy margins. The subscriber loss was distorted by Russia (700,000 accounts). Excluding that one-time hit, Netflix would have grown. The market was pricing in a structural decline that the financials didn't support.

-

Recognizing management's strategic pivot as a catalyst. Netflix's announcements of an ad-supported tier and a password-sharing crackdown weren't desperation moves—they were rational responses that would unlock massive revenue pools. The Microsoft partnership gave the ad tier credibility. These catalysts were identifiable within weeks of entry.

-

Understanding the "beat lowered expectations" dynamic. Netflix's own guidance for a 2 million subscriber loss in Q2 set an extremely low bar. Any result better than catastrophic would be reframed as "better than expected." The actual loss of 970,000—a beat of more than 1 million versus guidance—triggered the exit-week rally.

What Didn't Work

-

The drawdown was punishing. A -18.6% close-to-close drawdown (and -24.5% intraweek) would have shaken out most position traders. The stock spent 10 of the 13 weeks below the entry price. The trade required a tolerance for significant underwater time that most portfolios can't accommodate.

-

The +2.28% absolute return was thin for the risk taken. Sitting through a nearly 25% intraweek drawdown to capture a 2.28% return is a poor risk-reward outcome in isolation. The alpha against SPY makes it look better, but absolute return is what pays bills.

-

Macro headwinds limited the recovery. The June CPI shock and the Fed's 75bp rate hike created a hostile environment for any growth stock recovery. Netflix's company-specific catalysts were fighting against the strongest monetary tightening cycle in decades, capping the upside during the hold period.

-

Timing the exit was challenging. The Q2 earnings beat drove a sharp move from $189.11 to $220.44 in the exit week, but the intraweek high was $229.35. Capturing the full move required either holding through earnings or getting lucky with exit timing. A week earlier, the position was barely breaking even at $189.11.

Key Takeaways

-

Capitulation by high-profile investors can mark sentiment bottoms. Bill Ackman buying at $350+ and selling at $215 within three months—then publicly declaring he'd "lost confidence"—was a textbook capitulation signal. When sophisticated investors abandon positions at massive losses, it often signals that selling pressure is near exhaustion. Ackman's $400 million loss became a $3.4 billion missed gain by 2025.

-

Subscriber metrics can mislead when one-time factors dominate. Netflix's Q1 loss of 200,000 subscribers was real, but 700,000 of the shortfall came from Russia's forced shutdown. The market treated a geopolitical one-off as evidence of structural decline. Always decompose headline numbers before accepting the narrative.

-

Management pivots during crises deserve careful evaluation, not dismissal. The market initially scoffed at Netflix's ad-tier and password-sharing plans as "too little, too late." In reality, these initiatives would add tens of millions of subscribers and billions in revenue over the following two years. A crisis often forces management to pursue value-creating changes they would never have attempted during good times.

-

Alpha can matter more than absolute return in bear markets. The +2.28% absolute return looks modest, but generating +9.54% of alpha during a -7.26% market decline is meaningful. In a bear market, outperforming the index by nearly 10 percentage points—even with a small positive return—compounds powerfully over time.

-

Position sizing must account for maximum drawdown, not just expected return. This trade's -24.5% intraweek drawdown would have triggered margin calls or stop-losses for any position sized aggressively. The lesson is structural: post-earnings, high-volatility trades require smaller position sizes precisely when conviction feels highest, because the path to being right can pass through being very wrong first.

Sources

- Netflix Q1 2022 Earnings: Streaming Platform Loses Subscribers – Hollywood Reporter

- Netflix (NFLX) Earnings Q1 2022 – CNBC

- Netflix Loses 200,000 Subscribers in Q1, Predicts Loss of 2 Million More in Q2 – Variety

- Bill Ackman Sells Netflix Stake After Post-Earnings Plunge – CNBC

- Ackman's Pershing Square Gives Up on Netflix Stock, Taking $400 Million Loss – CNN

- Netflix Lost 970,000 Subscribers in Q2, Beating Its Estimate by More Than 1 Million Subs – Variety

- Netflix (NFLX) Earnings Q2 2022 – CNBC

- Netflix Loses Fewer Subscribers Than Forecast in the Second Quarter – NPR

- Netflix Could Introduce Ads, Crack Down on Password Sharing by End of Year – CNBC

- Bill Ackman Missed Out On $3.4 Billion Payday By Selling Netflix Stock Before the Boom – Benzinga

- How Rising Rates Could Influence Tech Earnings – CME Group

- Netflix Losing Streaming Dominance to Disney Plus, HBO Max, Apple TV Plus – Kiplinger